What’s Changed: 2018 Gartner Magic Quadrant for Data and Analytics Service Providers, Worldwide

-

By

Tim King

, Executive Editor at Solutions Review

By

Tim King

, Executive Editor at Solutions Review - Business Intelligence News,

Analyst house Gartner, Inc. has officially released its 2018 Magic Quadrant for Data and Analytics Service Providers, Worldwide. The report highlights full-service providers for consulting, managed services, and deployment for analytics and data management software. This Magic Quadrant features providers that support their customers’ specific use cases. Gartner adds: “These providers also offer services to support operational, tactical and strategic business decisions across products, customers and suppliers, as well as across business units and geographies.”

Service providers assist their customers in combining all the different elements related to a modern data and analytics deployment into a single portfolio. According to Gartner, its increasingly common for service providers to build and acquire software products, as well as maintain them. The report explains: “There is a deliberate strategy by service providers to offer data management platforms and analytics products as on-premises or as-a-service offers.

Artificial intelligence, namely data science and machine learning, play a key role in how the providers are ranked and positioned in the Magic Quadrant. This is not surprising, given the market’s shift toward automation and natural language processing technologies. The rapid increase in BI and analytics adoption, and the popularity of AI, is largely driven by the proliferation of data volumes amongst enterprise organizations.

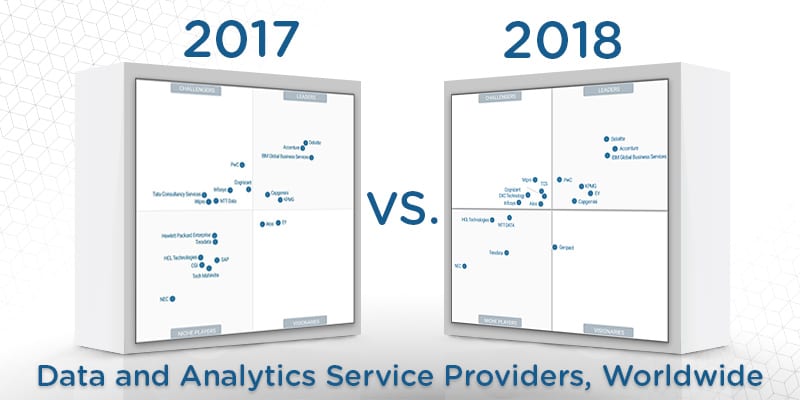

In this Magic Quadrant, Gartner evaluates the strengths and weaknesses of 18 providers that it considers most significant in the marketplace, and provides readers with a graph (the Magic Quadrant) plotting the vendors based on their ability to execute and their completeness of vision. The graph is divided into four quadrants: niche players, challengers, visionaries, and leaders. At Solutions Review, we read the report, available here, and pulled out the key takeaways.

DNX Technology and Genpact are the two newcomers in this year’s report. Tech Mahindra and SAP were axed for no longer meeting the inclusion criteria, specifically regarding revenue for the former. Hewlett Packard Enterprise (HPE) was removed due to the merging of its Enterprise Services with CSC into a new service organization called DXC Technology. CGI declined participation in the 2018 report and Gartner could not verify claims about inclusion criteria.

For the second-straight year, Deloitte, Accenture, and IBM Global Business Services are the three top players in the space. Deloitte distanced itself a bit from the pack with an increase in its vertical standing, though Accenture saw positive regression in its horizontal placement. PwC headlines the low left-hand cluster of vendors in this column, with its move from the challengers bracket last year. EY also made the leap to market leader from the visionaries column in 2017. Capgemini and KPMG round out the leaders quadrant.

Wipro and TCS made notable gains along Gartner’s completeness of vision axis and now find themselves as the class of the challengers quadrant. Cognizant’s position along the border of the leaders column saw no movement, and the provider remains a gust of wind away from massively upgraded standing next year. Atos made a major vertical move from the visionaries quadrant in 2017, now finding itself among the market challengers. The provider touts a broad set of products and skills, and a strong focus on innovation with its proprietary methodologies. DXC Technology and Infosys were also included in this field.

Genpact makes its debut as the only provider included in the visionaries quadrant. The company has recently re-positioned itself as a professional services firm with a strong focus on embedded analytics. Its portfolio is highlighted by a business outcome-focused approach, and the provider offers an industrialized analytics platform.

Though NTT Data took a but a tumble from its position amongst the market challengers in 2017, it remains the top dog in the niche players quadrant, slightly ahead of gainer HCL Technologies. NTT has expanded its service coverage and solution portfolio in recent months, and the company has a broad geographic reach. Teradata and NEC are also positioned as niche players, with neither showing much movement one way or the other over the last calendar year. The former focuses mainly on the financial services, retail, communications, manufacturing, and healthcare verticals.

That’s it for this year’s inclusions. However, Gartner chose to add an honorable mentions header at the bottom of this report, and included an additional listing of providers based on their specialty offerings. We encourage you to read the Magic Quadrant in full.

Read Gartner’s Magic Quadrant.

Related:

- Side-by-side BI and analytics product comparison guide

- 5 Business Intelligence and Data Analytics Vendors to Watch in 2018

- What’s Changed: 2018 Gartner Magic Quadrant for Data Management Solutions for Analytics

- What’s Changed: 2018 Gartner Magic Quadrant for Data Science and Machine-Learning Platforms

- What’s Changed: 2018 Gartner Magic Quadrant for Analytics and Business Intelligence Platforms

- What’s Changed: 2017 Gartner Magic Quadrant for Business Intelligence and Analytics Platforms

- Top 5 Questions to Ask When Evaluating BI & Data Analytics Software

Tim King

Executive Editor

Tim is Solutions Review's Executive Editor covering the human impact of AI on the future of work and learning. He is also the Media Strategist behind Insight Jam (1M+ on YouTube) events and programming. A 2017 and 2018 Most Influential Business Journalist and 2021 "Who's Who" in multiple categories, Tim is a recognized thought leader in enterprise tech and AI.

- Analytics and Data Science News for the Week of June 26; Updates from Databricks, Dataiku, WisdomAI & More - June 26, 2026

- Analytics and Data Science News for the Week of June 19; Updates from Databricks, Gartner, Qrvey & More - June 19, 2026

- Analytics and Data Science News for the Week of June 12; Updates from Databricks, Dataiku, Golden Analytics & More - June 12, 2026